Indian Startups are moving back home in 2026: The incredible reverse flip story that nobody is telling you

Not long ago, the standard playbook for any ambitious Indian startup was this: build in India, incorporate in Singapore or Delaware, raise money from global VCs, and aim for a NASDAQ listing. It was not just a preference. For many founders, it felt like the only viable path to serious capital and global credibility.

That playbook is being torn up. Indian startups are moving back home, and the movement has a name: reverse flipping. PhonePe did it. Groww did it. Zepto did it just before its IPO. Razorpay is in the middle of it. Meesho and Pine Labs are working on it. And the LinkedIn post that is circulating right now is just the visible tip of a much larger structural shift that has been building quietly for several years.

But here is what most of the coverage gets wrong: this is not a simple homecoming story. The full picture is messier, more interesting, and more instructive than a feel-good headline about Indian startups choosing India.

First, What Is the Reverse Flip?

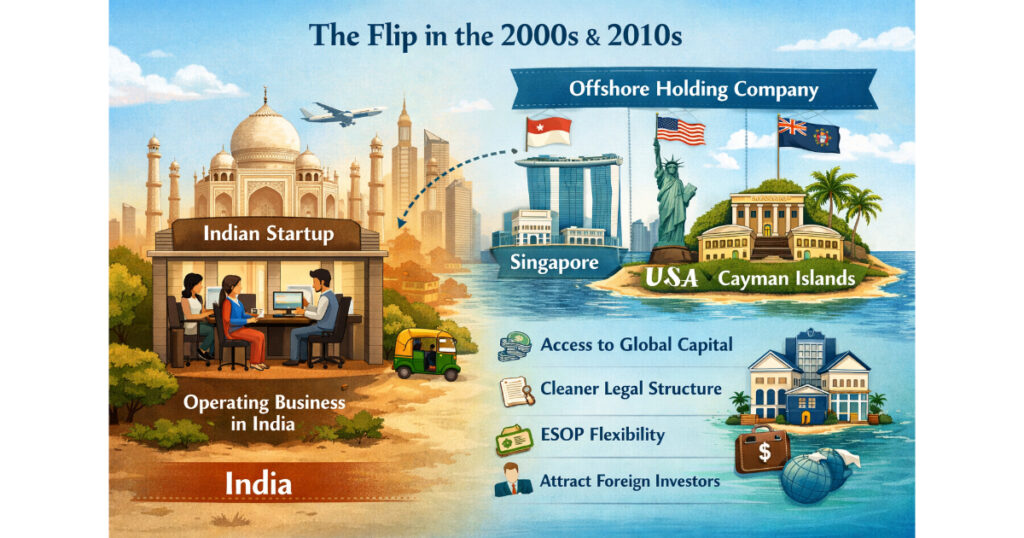

The original flip happened through the 2000s and 2010s. Indian founders incorporated their holding companies in foreign jurisdictions, most commonly Singapore, the United States, or the Cayman Islands. The operating business stayed in India, but the legal parent company sat offshore. This gave founders access to deeper capital markets, cleaner shareholder agreement frameworks, easier ESOP structuring, and the ability to attract foreign institutional investors who were often uncomfortable holding shares in Indian-incorporated entities.

The reverse flip, also called internalisation or gharwapsi, is the structural unwinding of that arrangement. The foreign holding company merges with or transfers its ownership to the Indian entity. India becomes the legal home of the group. The company can then list on Indian exchanges, the BSE or NSE, rather than on NASDAQ or the NYSE.

India is no longer just a place to launch a business. For a growing number of founders, it is now the place to scale, list, and build for the long term.

Who Has Actually Moved, Who Is Moving, and Who Has Paused

| Company | From | Status (as of March 2026) | Known Cost |

| PhonePe | Singapore | Completed | Rs. 8,000 crore in tax |

| Groww | USA | Completed | Approx. Rs. 1,340 crore |

| Zepto | Singapore | Completed (Jan 2025) | Not disclosed |

| Pine Labs | Singapore | NCLT approved, in process | Not disclosed |

| Razorpay | USA | In process | USD 100 million+ expected |

| Meesho | USA | Evaluating, paused | Not yet incurred |

| Udaan | USA | Paused as of Feb 2026 | Not yet incurred |

| KreditBee | Overseas | Paused as of Feb 2026 | Not yet incurred |

Sources: Business Standard, Aritra Partners, Asian Legal Business, various public filings. Costs are estimates or reported figures and may vary.

Why Startups Were Leaving India in the First Place

To understand why the reverse flip is happening now, it helps to remember why Indians startups left in the first place. This is often glossed over, but it matters.

Through the 2010s, India’s domestic capital markets were not meaningfully accessible to early-stage or growth-stage tech startups. SEBI’s listing norms were designed for traditional businesses, not loss-making, high-growth technology companies. Foreign VCs, particularly those writing Series A and Series B cheques, were often structured in a way that made investing in Indian-incorporated entities complicated. Shareholder agreement enforcement was uncertain. ESOP frameworks were cumbersome.

Singapore and Delaware solved all of these problems. A Singapore incorporation gave founders access to clean contract law, tax neutrality, straightforward shareholder agreements, and investors who were comfortable with the structure. It was not an emotional decision. It was a practical one.

The original flip was not about rejecting India. It was about accessing capital that was not yet available at home. That calculation has now changed.

What Actually Changed to Bring Them Back

Several things shifted at roughly the same time, and together they changed the cost-benefit calculation.

India’s IPO market matured fast

In 2024 alone, 62 IPOs raised USD 2.8 billion in Q1, accounting for 22% of global IPO activity. Companies like Swiggy, FirstCry, and Ola Electric listed on Indian exchanges and attracted strong domestic institutional and retail participation. For founders and investors who had been watching from their Singapore holding companies, this was hard to ignore. The exit route through Indian public markets was now genuinely viable.

Regulatory reform cut the timeline from 18 months to 90 days

In September 2024, the Ministry of Corporate Affairs amended Rule 25A of the Companies (Compromises, Arrangements and Amalgamations) Rules, introducing a fast-track reverse merger process. Under the new route, a foreign holding company can merge with its Indian wholly-owned subsidiary without requiring NCLT approval, subject to RBI clearance. This cut the process timeline from 8 to 18 months down to approximately 90 to 120 days. That is a meaningful operational change, not just a regulatory footnote.

GIFT City became a real alternative to Singapore

GIFT City, India’s international financial hub in Gujarat, now offers tax incentives, relaxed foreign exchange regulations, and infrastructure designed to compete with Singapore’s regulatory environment. As of 2025, approximately 60 fintech entities were registered within GIFT-IFSC. The IFSCA Listing Regulations introduced in 2024 also allow Indian companies to list internationally through GIFT-IFSC without requiring a domestic listing first. For founders who want global exposure without giving up Indian legal identity, this is a genuine option that did not exist three years ago.

India’s domestic investor base deepened

Family offices, domestic mutual funds, and retail investors are now active participants in growth-stage technology funding. The dependency on foreign VCs that once made offshore incorporation almost mandatory has reduced meaningfully, particularly for companies operating primarily in the Indian market.

The Part Nobody Talks About: It Costs an Enormous Amount to Come Home

Here is the part of the reverse flip story that tends to get buried under the patriotic framing.

PhonePe paid Rs. 8,000 crore in taxes to relocate from Singapore to India. That is approximately USD 960 million. Groww incurred approximately Rs. 1,340 crore in restructuring costs. Razorpay is expected to pay over USD 100 million for its move. These are not rounding errors. These are significant sums that companies paid to their government in order to bring their legal home back to the country where they already operated.

PhonePe paid Rs. 8,000 crore in taxes to come home. That is not a feel-good story. That is a company making a calculated long-term bet that Indian public markets will reward them more than the cost they paid to get there.

The tax implications arise because most reverse flip structures involve either share swaps or inbound mergers. In a share swap, shareholders of the foreign entity exchange their shares for shares in the Indian entity. This exchange is treated as a transfer and can trigger capital gains tax. The Tiger Global verdict from the Indian Supreme Court added further uncertainty around how foreign portfolio investors are taxed on such transactions, and this is one of the reasons several companies paused their reverse flip plans in early 2026.

ESOP restructuring adds another layer. Indian law governs employee stock options differently from US and Singapore law. When a company reverse flips, existing ESOPs issued under a foreign entity’s plan have to be cancelled and reissued under an Indian structure. This can create tax liability for employees at the point of cancellation, which requires careful planning and often legal and financial support for the employees affected.

Why Several Companies Paused in Early 2026

As of February 2026, several Indian startups including Meesho, Udaan, and KreditBee have put their reverse flip plans on hold. The reasons are specific and worth understanding individually rather than treating them as one story.

The selloff in Indian IT stocks through late 2025 and early 2026 weakened investor appetite for software and SaaS companies in particular. For companies that were planning to reverse flip in order to list on Indian exchanges, a weaker market for technology stocks means the valuation environment they were planning to list into has become less attractive.

The funding gap between India and the US for AI-focused startups is also relevant. In 2025, Indian AI companies raised USD 300 million across 98 rounds. US firms raised USD 122.5 billion across 849 rounds in the same period. For any startup with an AI angle considering where to be headquartered, those numbers are not easy to ignore.

The practical complexity of reverse flipping also tends to be underestimated in planning. Restructuring multi-jurisdictional corporate structures, renegotiating investor agreements, aligning ESOP plans, and obtaining regulatory clearances across two or more countries involves months of legal and financial work. Several founders have found that what looked like a 6-month project became an 18-month one, and pausing to reassess is a rational response to that reality.

What This Means for India’s Startup Ecosystem

The reverse flip trend, even with its current pause, reflects something real about where India’s startup ecosystem has arrived. The companies that have completed the move, PhonePe, Groww, Zepto, are paying the cost of the transition because they believe the Indian public market will deliver better long-term outcomes for them than a foreign listing. That is not a sentiment play. That is a financial calculation backed by the performance of Indian exchanges and the depth of domestic investor participation.

For Indian retail investors, this matters directly. When a company like Groww reverse flips and lists on Indian exchanges, Indian investors can buy shares in it through a regular Demat account. When it was a US-incorporated entity, those shares were not easily accessible to domestic retail participants. The return of Indian-origin companies to Indian markets expands the investable universe for ordinary Indian savers.

For the government, the tax revenue from these transitions is significant. PhonePe’s move alone contributed approximately Rs. 8,000 crore to government revenues. Razorpay’s planned move is expected to contribute over Rs. 1,600 crore. Multiply that across the estimated 90% of foreign-domiciled Indian unicorns that industry estimates say will eventually reverse flip, and the fiscal impact is substantial.

The Honest Assessment

India has earned this trend. The improvements to SEBI’s listing framework, the Companies Act amendments, the development of GIFT City, and the maturation of domestic capital markets are all real. The reverse flip is not just sentiment. Companies are paying billions of rupees in taxes to come home, which is the most concrete vote of confidence possible.

At the same time, the pause in early 2026 is a reminder that this process is not automatic or irreversible. The conditions that make India attractive for a reverse flip, a strong IPO market, clear tax treatment, a deep domestic investor base, are conditions that have to be maintained and improved continuously. The Tiger Global tax uncertainty, the IT stock selloff, and the US funding advantage in AI are all signals that India cannot afford to take this homecoming trend for granted.

The Indian startups that have already moved are now fully invested in the country’s success. The ones still watching from Singapore and Delaware will make their decisions based on what they see happen next. That is, ultimately, what competition for corporate domicile looks like. And right now, India is winning more of those decisions than it ever has before. The question is whether it can make the conditions permanent rather than cyclical.